By Simon Whitten, Jonathan Chandler, CFA, and James Fifield, CFA on

COVID Concerns Cause Headwind for Alternative Weight

As has been the case since the pandemic began, performance of Alternative Weight strategies in Q2 was largely driven by business risk factors. Those industries aligned with the stay-at-home theme (Information and IT) diverged from those aligned with re-opening themes (tourism, energy and value stocks in general). However, several new themes emerged with strong performance in the second quarter, notably infrastructure-related stocks and those with significant recurring revenues outperformed, which may signal defensive positioning.

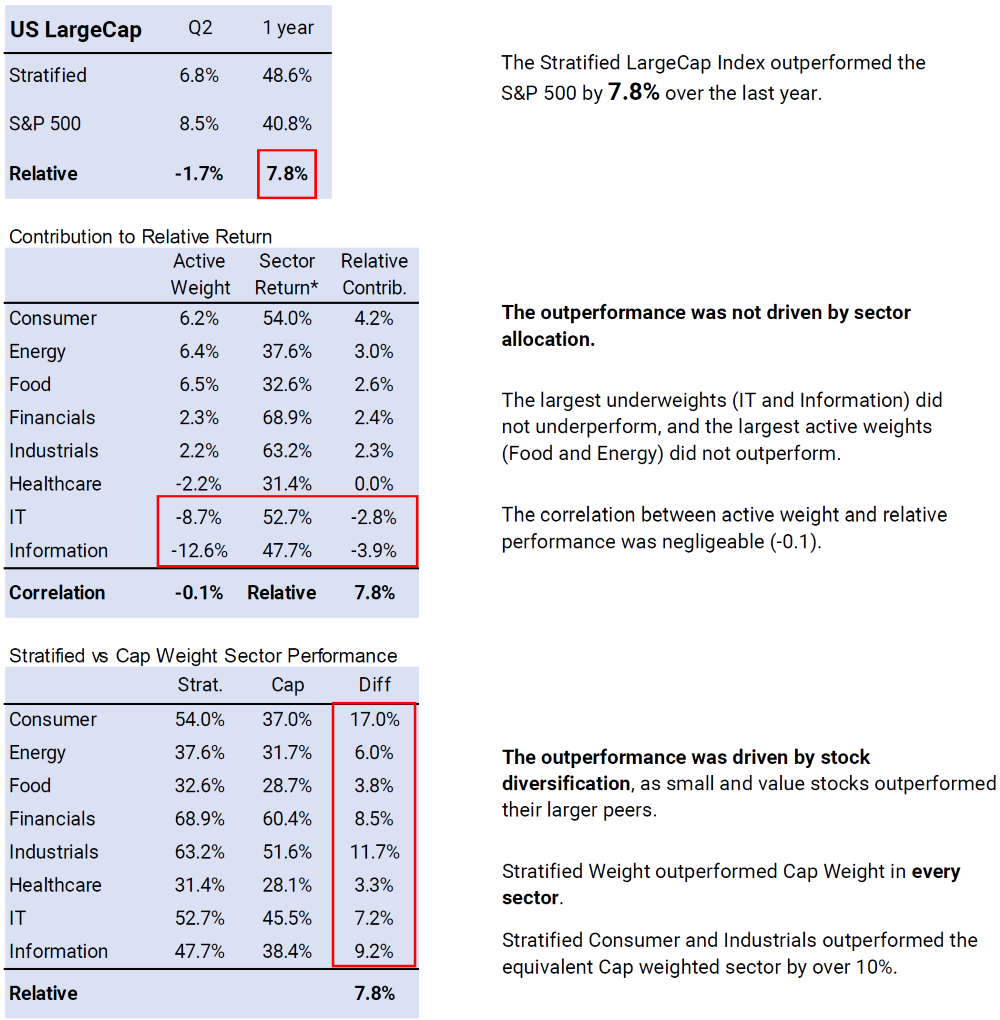

After a strong last twelve months for Alternative Weight (which typically has a significant exposure to value), cap weight outperformed in Q2. Infection rates remain worryingly high in several countries and the reopening trade became less attractive from a valuation perspective as investors showed a renewed interest in technology stocks. The S&P 500 rose 8.5% for the quarter, outperforming the S&P 500 Equal Weight Index by 1.6% and the Stratified LargeCap Index by 1.7%.

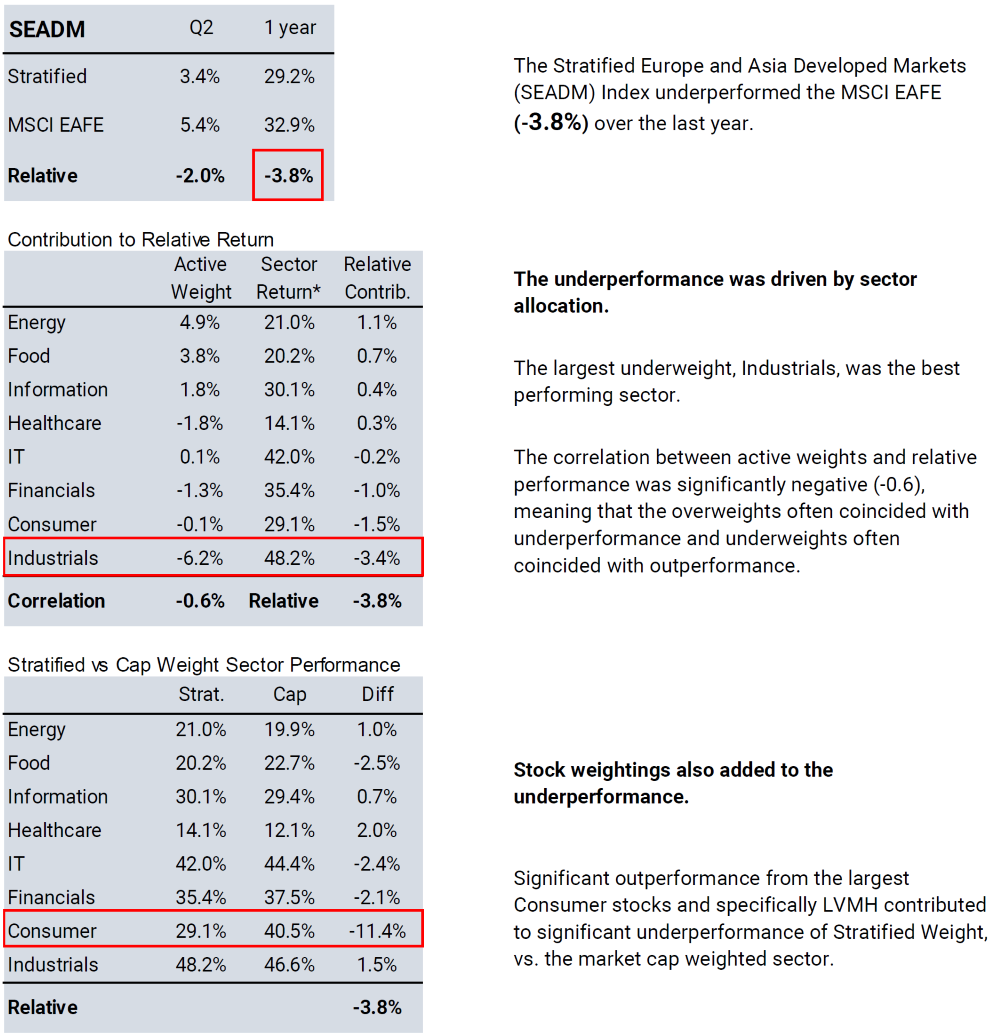

A similar dynamic was seen internationally, with the MSCI EAFE index rising 5.4% in Q2 and alternative weight underperforming by 2% (MSCI EAFE Equal Weighted rose 3.5% and its Stratified Weight counterpart, SEADM rose 3.4%).

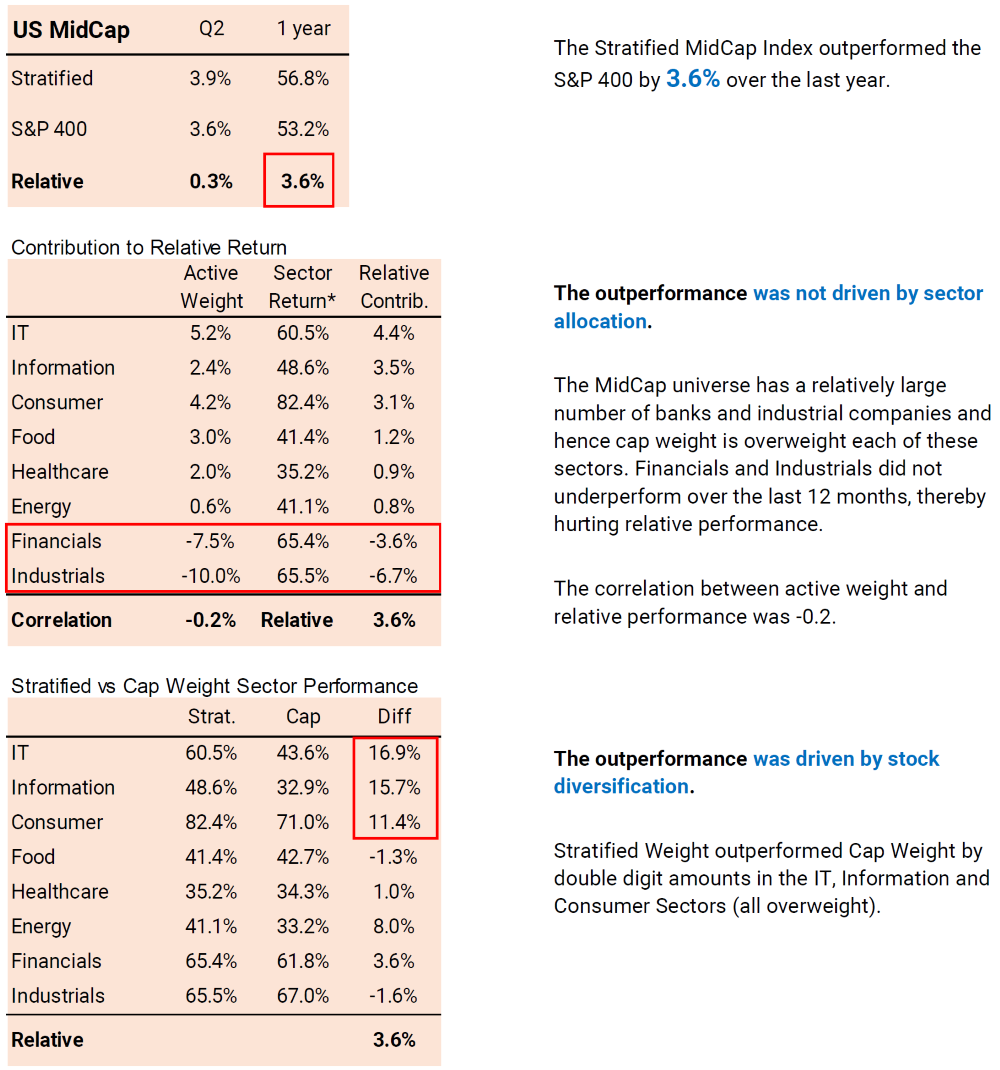

Small and midcap stocks continued to rise in Q2 (the S&P 400 rose 3.6% and the S&P 600 rose 4.5%). Stratified Weight indices marginally outperformed their cap-weighted counterparts, with the Stratified MidCap and SmallCap rising 3.9% and 4.9%, respectively.

Exhibit 1. Core Index Comparison Source: Syntax, S&P Dow Jones Indices, MSCI. Total return performance does not reflect fees or implementation costs as an investor cannot directly invest in an index. 12-months covers period from 6.30.2020 to 6.30.2021. * Syntax Stratified Europe & Asia Developed Markets Index, based on the MSCI EAFE universe. The performance differential between cap- and alternatively-weighted indices was driven by differences in the sector and stock weighting methodologies. Cap weight has large stock concentrations which in turn lead to uncontrolled sector weightings. Equal weight indices have diversified stock positions, but do not control for sector biases. Stratified Weight is designed to control for sector concentrations and diversifies stock positions within similar industries (see Exhibit 2). This can lead to significant relative performance differentials given the wide sector divergences.

Exhibit 2. Weighting Methodologies

For illustration purposes only.Sector Performance

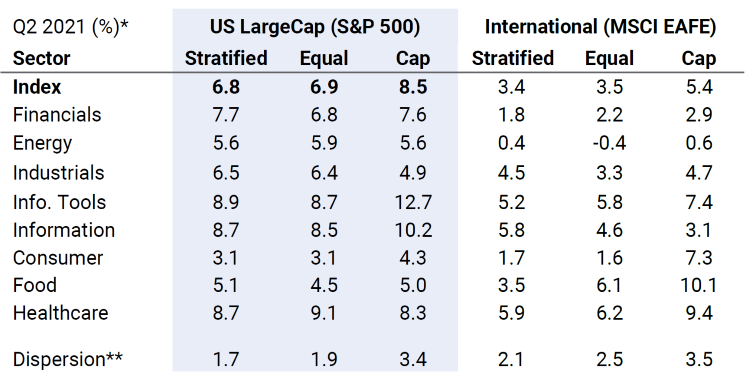

Following several months of underperformance, IT stocks performed well (+4.2% vs S&P 500 and +2.2% vs MSCI EAFE) as did other “Pandemic beneficiaries”, such as Healthcare and Information. On the other side of the trade, the more cyclical and travel sensitive Energy (-2.9% vs S&P 500) and Consumer (-5.3% vs S&P 500) sectors were among the worst performers as valuations have become less compelling.

Exhibit 3. Q2 Sector Performance by Weighting Methodology Source: Syntax, S&P Dow Jones Indices, MSCI. * Total return performance does not reflect fees or implementation costs as an investor cannot directly invest in an index. **Dispersion is the cross-sectional standard deviation of sector returns.

Trending and Emerging Sectors and Industries

We highlight the established trends and those groups that are turning in Exhibit 4 below. Performance of all broad sectors and industry groups in across different US size segments and internationally is shown at the end of this piece.

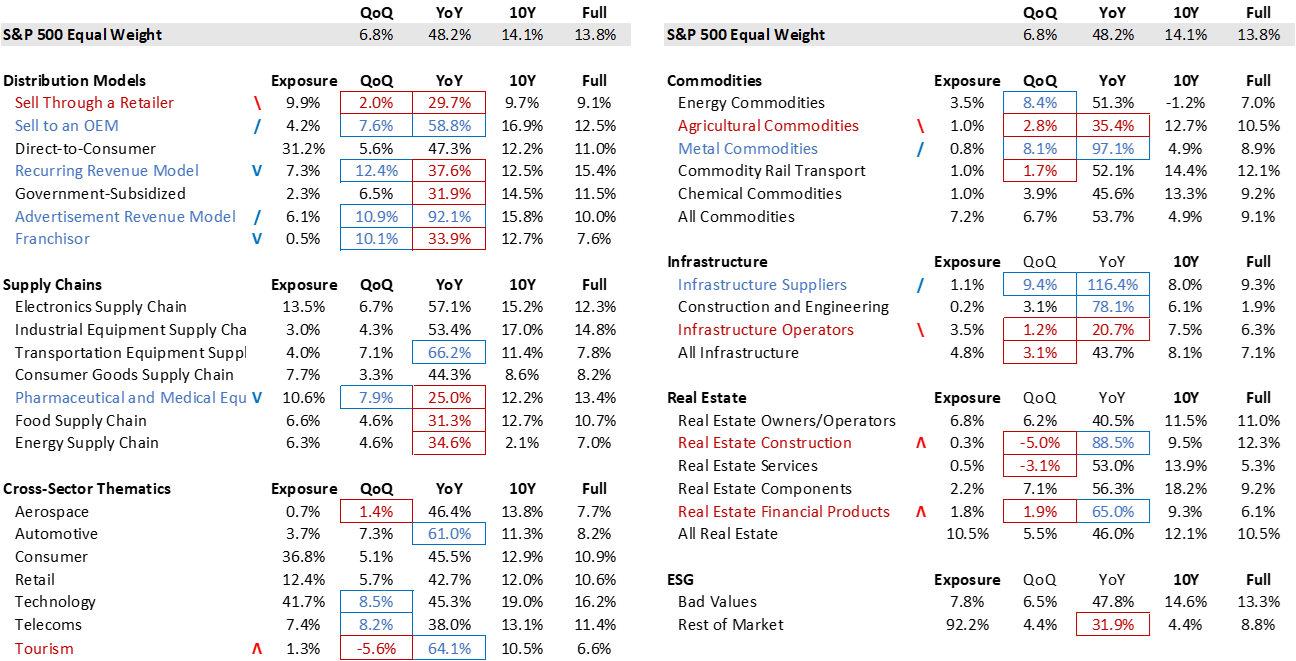

The strong global performance of Apparel stocks over the past 12 months has propelled LVMH to become the 4th largest stock in the MSCI EAFE index (as of June 30th). Interestingly, this trend has broken down in the US, where Apparel stocks underperformed the market in Q2. We also noticed a divergence in the performance of Banking stocks, as US banks began to outperform and international banks underperformed in Q2.

“Stay at home” groups like Software, Internet Services and Pharmaceuticals outperformed globally in Q2, having underperformed during the previous nine months, while Gas and Electric utilities underperformed in every size segment and both regions.

Exhibit 4. Trending and Emerging Industries Source: Syntax Affinity™

Identifying Themes with Affinity™

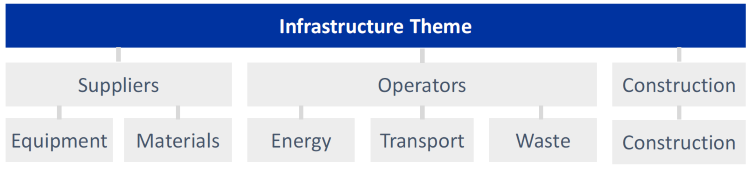

Syntax Affinity™ uses a multi-attribute classification system to view a portfolio or index from multiple perspectives. By applying different thematic lenses, Affinity™ calculates the portfolio exposure and performance for a number of cross-sector themes. These themes can be industry-based, like Tourism, or commodity-based, considering not only commodity providers, but companies involved with the entire supply chain for that commodity, or could involve any combination of business risks, e.g. companies with recurring revenues.

Stocks which contain relevant thematic attributes are sorted into homogenous groupings and organized into hierarchies from which portfolio exposures and thematic performance can be calculated. For example, the Infrastructure Theme is shown in exhibit 5.

Source: Syntax Affinity™

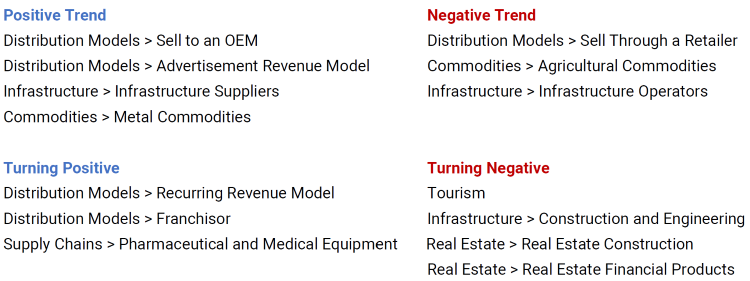

Trending and Emerging Themes

Affinity™ calculates the aggregate performance of all stocks in a particular thematic group.

In Q2, infrastructure suppliers (e.g. Caterpillar, United Rentals, Vulcan Materials) rose 9.4% as the Democrats continued to push their $1.2 trillion infrastructure spending plan. This was in contrast to infrastructure operators (utilities, waste management, rail etc) which underperformed (+1.2% in Q2).

The best performing theme in the second quarter involved stocks with recurring revenue models (including software and REITs). This may signal that investors are focusing more on cashflow stability than growth.

Following a strong rebound in the last 12 months, Tourism was the worst performing theme in the second quarter (-5.6%), with all subgroups (airlines, cruises, hotels, casinos and booking websites) underperforming. The groups were hurt by a rise in new infections globally and this pull back follows three quarters of significant outperformance (Exhibit 6).

Exhibit 6. Trending and Emerging Themes Source: Syntax, Affinity™ “Trending” themes under/outperformed in Q2 and have under/outperformed for the last 12 months. “Turning” themes under/outperformed in Q2, but out/underperformed for the last 12 months (Exhibit 6). Exhibit 7. Thematic Performance and Exposure within the US LargeCap Universe Source: Syntax, Affinity, S&P Dow Jones Indices. Performance is calculated as the weighted average total return of the subset of the S&P 500 Equal Weight Index constituents who are members of the Affinity Theme. QoQ shows total return for 3.31.21 to 6.30.21. YoY shows total return from 6.30.20 to 6.30.21. Full performance period uses period from 12.31.1991 when available. Performance does not reflect fees or implementation costs.

Dissecting Stratified Weight Performance

Stratified LargeCap Index relative to S&P 500 sector attribution Source: Syntax, Factset. Contribution to Relative Return and Sector Performance tables are based on 12 months from 6.30.20 to 6.30.21. * Sector Return is the 1-year total return of the Stratified Weight sector. Correlation is the cross-sectional correlation between active weight and sector return. Performance does not reflect fees or implementation costs. SEADM Index relative to MSCI EAFE sector attribution Source: Syntax, Factset. Contribution to Relative Return and Sector Performance tables are based on 12 months from 6.30.20 to 6.30.21. *Sector Return is the 1-year total return of the Stratified Weight sector. Correlation is the cross-sectional correlation between active weight and sector return. Performance does not reflect fees or implementation costs.

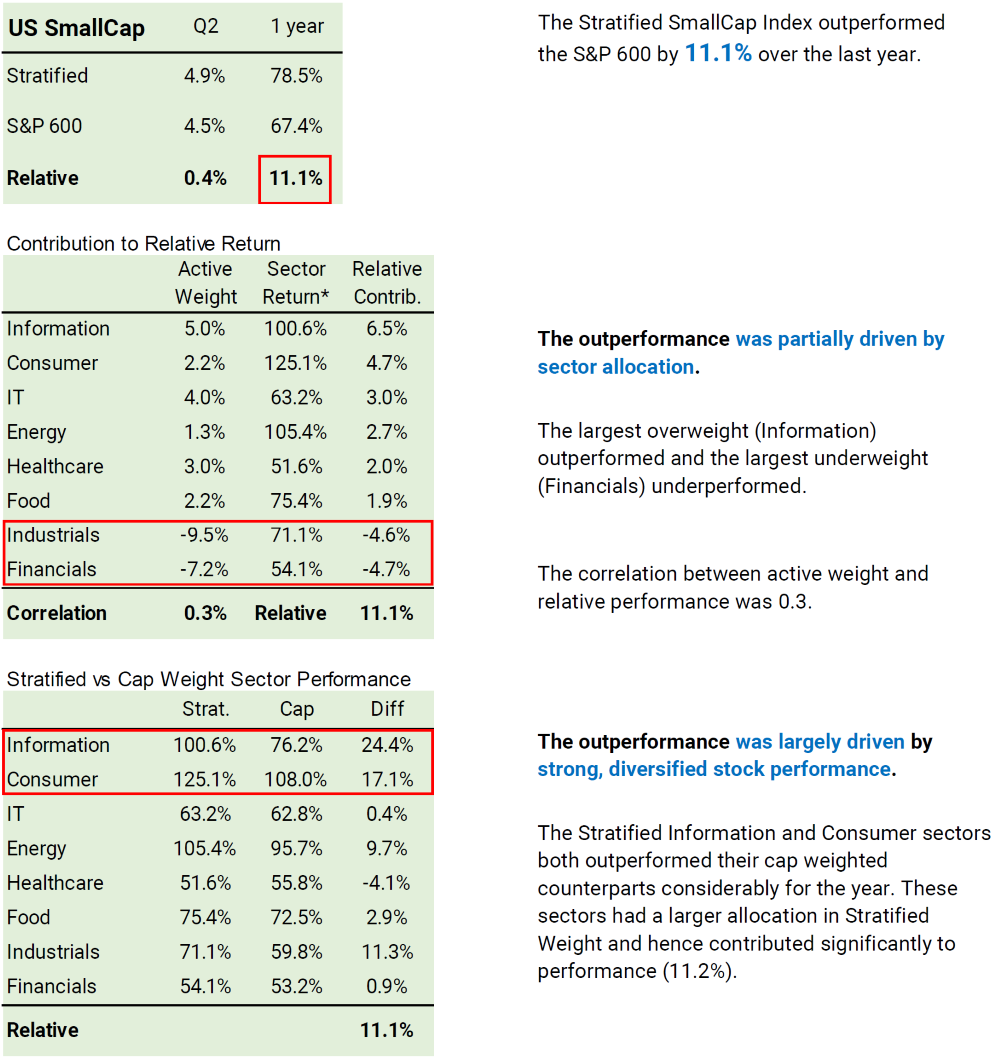

Stratified MidCap Index relative to the S&P MidCap 400 Source: Syntax, Factset. Contribution to Relative Return and Sector Performance tables are based on 12 months from 6.30.20 to 6.30.21. *Sector Return is the 1-year total return of the Stratified Weight sector. Correlation is the cross-sectional correlation between active weight and sector return. Performance does not reflect fees or implementation costs. Stratified SmallCap Index relative to the S&P SmallCap 600 Source: Syntax, Factset. Contribution to Relative Return and Sector Performance tables are based on 12 months from 6.30.20 to 6.30.21. *Sector Return is the 1-year total return of the Stratified Weight sector. Correlation is the cross-sectional correlation between active weight and sector return. Performance does not reflect fees or implementation costs.

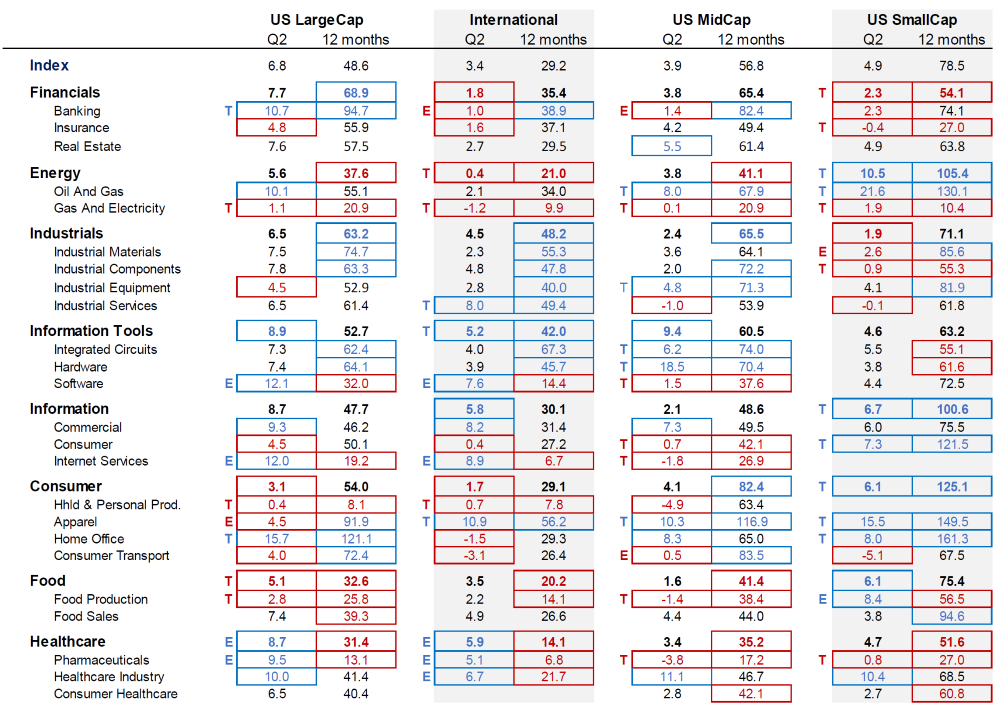

Sector performance for Stratified US size segments and Stratified International universes Source: Syntax, Affinity™. T denotes positive (blue) or negative (red) trends for Q2 and 12 months relative returns. E denotes evolving trend (different Q2 and 1 year). Boxes highlight top and bottom ten groups in each universe/time period. Performance does not reflect fees or implementation costs.

Important Disclaimers

This document is for informational purposes only and is not intended to be, nor should it be construed or used as an offer to sell, or a solicitation of any offer to buy, any security. Additionally, the information herein is not intended to provide, and should not be relied upon for, legal advice or investment recommendations. You should make an independent investigation of the matters described herein, including consulting your own advisors on the matters discussed herein. In addition, certain information contained in this factsheet has been obtained from published and non-published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such information is believed to be reliable for the purpose used in this factsheet, such information has not been independently verified by Syntax and Syntax does not assume any responsibility for the accuracy or completeness of such information. Syntax LLC, its affiliates and their independent providers are not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein.

Past performance is no guarantee of future results. The inception date of the Syntax Stratified LargeCap and Syntax Stratified MidCap Indices was December 27, 2016. The inception date of the Syntax Stratified SmallCap Index was January 3, 2020. The inception date of the Syntax Europe & Asia Developed Markets (“SEADM”) Index was January 1, 2016. The inception date of the Syntax Real Asset Index was July 1, 2015. Charts and graphs are provided for illustrative purposes only.

Index performance does not represent actual fund or portfolio performance and such performance does not reflect the actual investment experience of any investor. An investor cannot invest directly in an index. In addition, the results actual investors might have achieved would have differed from those shown because of differences in the timing, amounts of their investments, and fees and expenses associated with an investment in a portfolio invested in accordance with an index. None of the Syntax Indices or the benchmark indices portrayed herein charge management fees or incur brokerage expenses, and no such fees or expenses were deducted from the performance shown; provided, however that the returns of any investment portfolio invested in accordance with such indices would be net of such fees and expenses. Additionally, none of such indices lend securities, and no revenues from securities lending were added to the performance shown.

The Syntax Stratified LargeCap Index, Syntax Stratified MidCap Index, Syntax Stratified SmallCap Index, SEADM Index are the property of Syntax, LLC, which has contracted with S&P Opco, LLC (a subsidiary of S&P Dow Jones Indices LLC) to calculate and maintain the Indices. The Indices are not sponsored by S&P Dow Jones Indices or its affiliates or its third party licensors (collectively, “S&P Dow Jones Indices”). S&P Dow Jones Indices will not be liable for any errors or omissions in calculating the Index. “Calculated by S&P Dow Jones Indices” and the related stylized mark(s) are service marks of S&P Dow Jones Indices and have been licensed for use by Syntax, LLC. S&P® is a registered trademark of Standard & Poor's Financial Services LLC (“SPFS"), and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). The MSCI EAFE Index was used by Syntax, LLC as the reference universe for selection of the companies included in the SEADM Index. MSCI does not in any way sponsor, support, promote or endorse the Index. MSCI was not and is not involved in any way in the creation, calculation, maintenance or review of the Index. The MSCI EAFE Index was provided on an “as is” basis. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating the MSCI EAFE Index (collectively, the “MSCI Parties”) expressly disclaim all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non‐infringement, merchantability and fitness for a particular purpose). Without limiting any of the foregoing, in no event shall any of the MSCI Parties have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages in connection with the MSCI EAFE Index or the SEADM Index. Prior to March 19, 2018, the SEADM Index was calculate by NYSE. Sector subsets of the Syntax Stratified LargeCap, Syntax Stratified MidCap, and SEADM Indices are calculated using model performance generated in FactSet, and as such may differ from index calculations performed by S&P Dow Jones Indices. The Affinity Thematics are the property of Syntax, LLC, which has calculated their performance using Affinity™. Syntax will not be liable for any errors or omissions in calculating the Affinity Thematics. Syntax®, Stratified®, Stratified Indices®, Stratified-Weight™, Stratified Benchmark Indices™, Stratified Sector Indices™, Stratified Thematic Indices™, Affinity™, and Locus® are trademarks or registered trademarks of Syntax, LLC and its affiliate Locus LP.

The S&P 500® Index is an unmanaged index considered representative of the US mid- and large-cap stock market. The MSCI EAFE Index is an unmanaged index considered representative of the European, Australian, and East Asian large-cap stock market. Benchmark data for the S&P 500, S&P 500 Equal Weight, S&P MidCap 400, S&P MidCap 400 Equal Weight, S&P SmallCap 600, S&P SmallCap 600 Equal Weight, and S&P Real Assets Equity Indices are provided by S&P Dow Jones through FactSet®. Benchmark data for the MSCI EAFE index is provided by MSCI through FactSet.