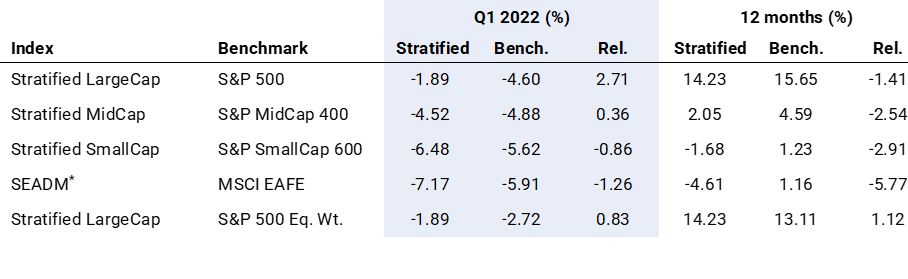

Major benchmarks fell in Q1, Stratified LargeCap outperformed

Following a particularly strong fourth quarter of 2021, equity markets have struggled to maintain their momentum this year. The Russia-Ukraine conflict, coupled with higher bond yields caused a strong headwind for growth assets, especially those which are market cap weighted. In Q1 2022, the S&P 500 fell 4.60%; MSCI EAFE fell 5.91% and the S&P SmallCap 600 fell 5.62%.

The Stratified US LargeCap Index outperformed both the cap-weight and equal- weight S&P 500 benchmarks (by 2.71% and 0.83% respectively; see Exhibit 1). This outperformance was due to greater business risk diversification, which resulted in relatively lower exposure to poorly performing growth segments (which are overweighted in the S&P 500) and relatively higher exposure to the strongly performing Energy and value stocks, which are under-represented in the S&P 500.

Exhibit 1. Core Index Comparison

Rising inflation drives a business risk rotation

Equity markets appear to have largely discounted the long-term effects of the Pandemic, with the S&P 500 approximately 25% above its pre-COVID peak in February 2020. However, rising instability in the form of persistently high commodity prices due to the Russia-Ukraine war, coupled with COVID-related staffing shortages and supply chain bottlenecks, caused an inflation shock that rattled global markets this year.

Inflation is often a symptom of economic instability. With inflation looking less transient than the market and the Fed had previously predicted, investors are rotating into inflation-sensitive or inflation-hedging equities. Using the Affinity™ engine, we calculate the performance of hundreds of business groupings. By isolating inflationary periods over the past twenty years, we find that the groups that are most likely to outperform during an inflation market regime are, unsurprisingly, those with direct involvement with the extraction of commodities. Indeed, the Affinity ‘Resource Extraction’ Activity, which includes companies in the business of extracting Oil, Metals, Lumber and any other natural resource is the best performing group during inflationary periods (Exhibit 2). Since the group spans multiple sectors (e.g. Energy, Industrials and Materials in GICS), it is difficult to measure using traditional classification systems.

This year, as the inflation rate rose from 7.0% to 8.5%, an equally weighted basket of Resource Extraction companies returned 31.76%.

Exhibit 2: The most inflation sensitive groups in the S&P 500

Regime Shift from Growth to Value continues

As a result of rising inflation, US bond yields have risen precipitously in 2022, with the flagship US 10-year bond yield nearly doubling from 1.5% at the start of the year to 2.9%. As we wrote in our recent note, “Regime Shifts - Why the S&P 500 could underperform Alternative Weighted ETFs”, a rise in interest rates has a profound effect on the relative fortunes of Growth stocks, and in turn the performance of cap versus alternatively weighted indices.

Higher interest rates are often a headwind for growth companies, since Growth stocks often rely on future earnings potentially more than their Value counterparts, hence they have a higher sensitivity to changes in the discount rate. When interest rates rise, their future earnings are discounted heavily and therefore earnings are downgraded more for Growth names than Value ones. The oversized weight of Tech (growth) within the S&P 500 means that any underperformance of Growth stocks will lead to underperformance of cap weight vs alternatively weighted products (as evidenced by the strong correlation in Exhibit 3). This year the S&P 500 Value index has outperformed the S&P 500 Growth index by 15.0% and the Syntax Stratified LargeCap index has outperformed the S&P 500 index by 5.7% (to 4.28.2022).

Exhibit 3: S&P 500 recently underperforms as Value outperforms

We note that the style biases that are so pronounced in the US LargeCap universe are not prevalent in other regions or size segments, where tech is far less dominant. We believe that a significant value exposure explains why the MSCI EAFE and the S&P 600 have fared better in relative terms versus their alternatively weighted counterparts so far this year.

Market turbulence drives renewed interest in defensive equities

The recent market volatility stemming from the Russia-Ukraine conflict amidst rising interest rates has prompted stocks in selective defensive groupings to outperform in Q4 2021 and 2022 (Exhibit 4).

Exhibit 4: Performance of the Affinity Defensive Theme in S&P 500

Stratified Weight Indices have a consistently higher allocation to defensive business risks (Exhibit 5) due to their diversified methodology which does not favor any one sector or industry (such as technology in the S&P 500 or Industrials in MSCI EAFE).

Exhibit 5: S&P 500 Exposure to Defensive Equities

The result is that Stratified Weight has less cyclicality and a higher weight in the defensive business groupings for all our major regions and size segments (Exhibit 6).

Exhibit 6: Core Benchmark Exposure to Defensive Equities

Conclusion

The decline in the S&P 500 this year has been attributed to (amongst other things) stress from the Russia-Ukraine conflict and rising inflation and interest rates. We believe that historically high levels of concentration, due to the cap weighted index methodology is exacerbating the decline.

The index is not only overexposed to Technology-related business risks, but also by extension overexposed to rising interest rates, inflation, the business cycle and unrealistic earnings expectations.

Now more than ever, we believe that the S&P 500 is taking diversifiable risks in its attempt to capture the market equity risk premium and that a more diversified index, namely the Stratified LargeCap Index offers a better representation of the broad market for those investors wishing to invest in equities without taking an outsized view on any sector, industry or company.

%20(Small).png)

.png)

.png)

.png)

.png)