Syntax Creates New ESG Index that Aims to Improve Portfolio Outcomes

2019 was a record year for ESG fund inflows and 2020, despite market turmoil, is shaping up to continue that trend. In the first quarter of 2020, sustainable ETFs added a net $7.8 billion, accounting for 40% of all equity ETF flows. ESG mutual funds saw $2.7 billion of net inflows during the quarter, even as broader equity mutual funds had net outflows of $5.7 billion [1].Syntax joins this momentous shift with an innovative ESG index built to improve upon best practices in passive ESG integration. On July 31st, Syntax launched the Stratified LargeCap ESG Index, which seeks to provide broad coverage of large-cap U.S companies while tilting exposure towards the companies that outperform their peers on material ESG metrics. The index uses Syntax’s patented stratified weight methodology to control for business risk and improve diversification.

While the Syntax Stratified LargeCap ESG Index was developed as an institutional solution with limited negative screening for business involvement and considers only material ESG risks, the index can serve as a basis for values-driven portfolio customization, such as fossil-fuel exclusions, or tilts towards certain impact themes, including one or more of the UN Sustainable Development Goals. Further, the business risk diversification provided by stratified weight can help improve risk-adjusted returns in these custom strategies.

The Syntax Stratified LargeCap ESG Index differentiates itself from other offerings with four features:

a transparent and rules-based environmental and social scoring methodology;

a rules-based materiality model informed by Syntax’s Functional Information System (FIS) data;

a consistent approach to governance;

and business risk diversification

In this piece, we will discuss each of these distinguishing features of the Syntax Stratified LargeCap ESG index.

Transparent and Rules-Based Scoring Methodology

Passive investment strategies should follow a clear set of rules that are made available to investors and the public through a methodology document. Factor indices, for example, typically implement screens to exclude companies from the index if they do not meet defined criteria, such as price to book ratio, and the details for implementing those screens are published in methodology documents. For less straightforward factors, like quality, for which there is no consensus definition, the methodology document serves to define the factor and the formula used to calculate it.

ESG indices typically aggregate large sets of environmental, social and governance data on each company to arrive at a total ESG score and will exclude and/or weight constituents based on that ESG score. Very often, however, the calculation of this ESG score is obscured. Moreover, the ESG scoring methodologies often leave room for analysts to make ad hoc determinations in the scoring process. The result is a strategy similar to a black-box active approach that does not disclose the decision-making process [2].

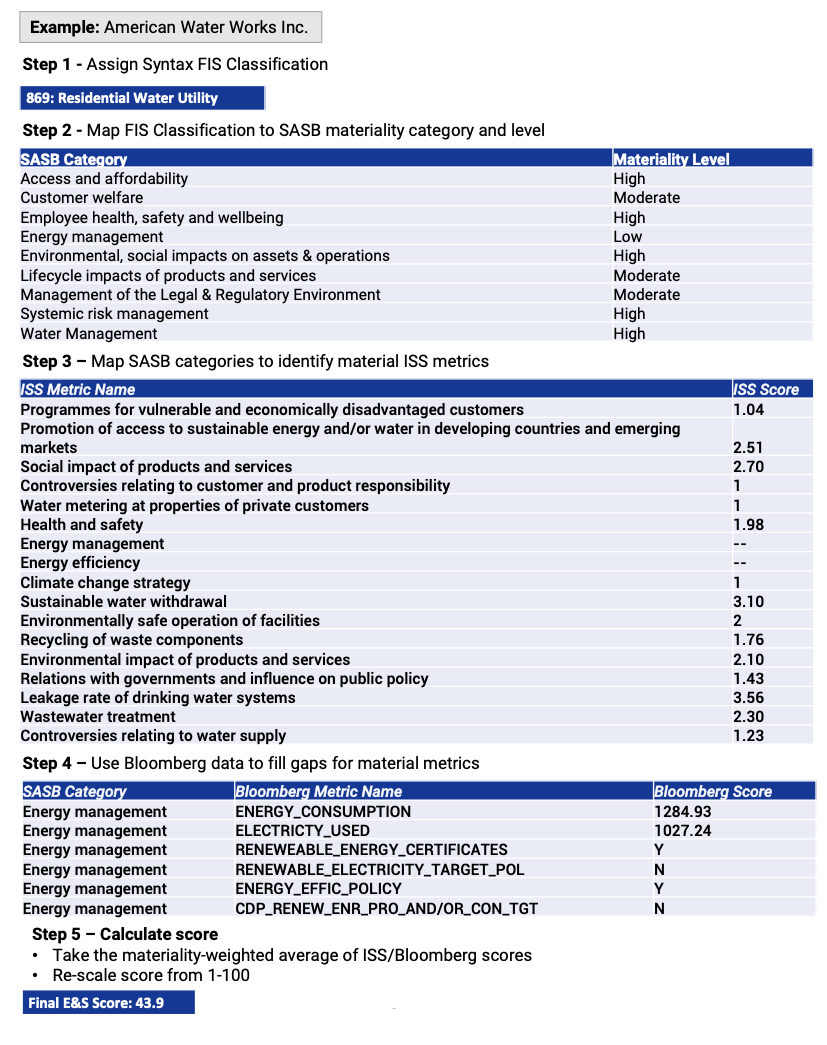

The Syntax Stratified LargeCap ESG Index follows a standardized, rules-based methodology for applying ESG scores and makes that methodology publicly available at a granular level. To determine ESG scores, Syntax uses third-party ESG data from ISS and Bloomberg mapped to the widely accepted and publicly available Sustainability Accounting Standards Board (SASB) materiality framework. After extensive ESG data provider due diligence that included discussions with at least seven of the major ESG data providers, Syntax selected ISS and Bloomberg ESG data not only for the quality of their data, but their granularity and transparency, which allows Syntax to communicate to investors exactly what datapoints drive a company’s ESG score. The result is a more transparent, rules-based approach to ESG that is more consistent with the values of passive investing. See Exhibit 1 for a demonstration of the Syntax ESG scoring process.

Others have taken note of the lack of transparency around passive ESG. In July 2019, State Street Global Advisors launched their R-Factor scoring system that hopes to become a more transparent standard for ESG scoring. While, the R-Factor approach differs from the Syntax approach in scoring methodology, we applaud efforts towards this end.

Rules-Based Materiality

Further contributing to the rules-based nature of Syntax’s approach to ESG is Syntax’s FIS classification system, which allows for an algorithmic approach to materiality compared with the ad hoc materiality assessments of other ESG scoring systems like those used by MSCI, which can lead to inconsistencies across companies and industries as well as a lack of transparency into the metrics driving company scores. The Syntax Stratified ESG Index leverages Syntax’s patented FIS industry classification system to precisely pinpoint material ESG metrics. A core tenant of institutional ESG investing is to consider only the environmental and social risks that are material to a company’s financial performance. For example, water management should not materially impact the operations of a company like Bank of America, but it is critical for the operations of a company like Newmont Mining Corp. that operates in a water-intensive industry. Numerous frameworks have been developed to try and determine which environmental and social topics are material for which industry, but SASB has emerged as the most widely used framework both by corporations for financial reporting and by investors for financial analysis.

Exhibit 1: Source: Syntax. Scores shown are for illustration purposes only

Syntax sees value, both for transparency and for standardization purposes, in using a widely adopted materiality framework such as SASB. However, we see evidence that the industry classification systems currently used to determine what environmental and social topics are material for each industry can be improved. The Syntax ESG index’s approach to materiality builds on a paper by Decio Nascimento, CIO at Richmond Global Compass, presented at the Yale School of Management in October 2018, which points to the need for a better industry classification system to determine ESG materiality. Syntax leverages the granularity, flexibility and logicality of its FIS classification system to better identify material ESG risks. Syntax FIS has over 5,000 summary classifications containing over 100,000 component tags. This level of granularity allows us to isolate the characteristics of each company’s business model that correspond with a particular ESG risk category. For more information on Syntax FIS visit syntaxindices.com.

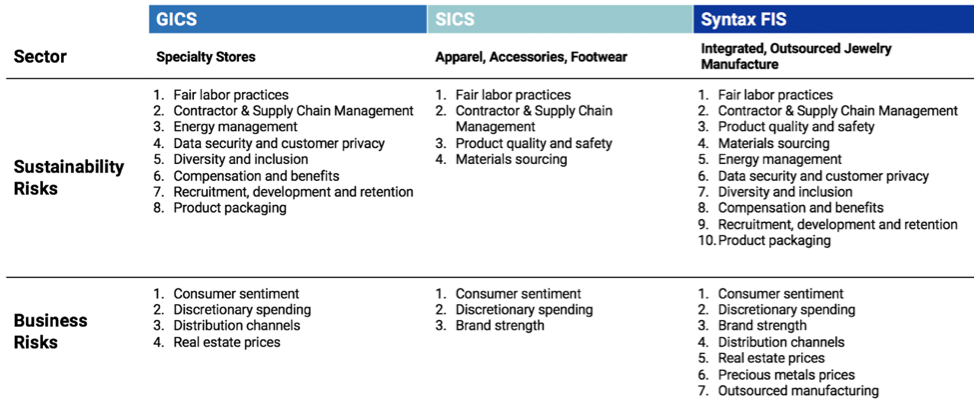

FIS is also a highly flexible classification system. In contrast to other classification systems, which are arranged in static hierarchies, FIS is a multi-dimensional tagging system that allows Syntax to capture a range of risk perspectives, including sustainability risks. Exhibit 2 shows the Syntax FIS classification of Tiffany & Co. compared with 2 other classification systems, GICS and SICS. The first classification system, GICS, places Tiffany into a Specialty Stores group—a retail classification—and the second classification system, SICS, places it into Apparel, Accessories, Footwear — a manufacturing classification. Syntax FIS classifies Tiffany as Integrated, Outsourced Jewelry Manufacture, which captures both Tiffany’s manufacturing and retail functions. This, in turn, allows us to consider the sustainability risks associated with both functions. Similarly, Syntax FIS can better capture a host of risks to Tiffany’s operations—what we call business risks—and control for those risks via stratified weight.

Exhibit 2: Example FIS Classification for Tiffany & Co. FIS Classification of Tiffany & Co. Sources: GICS via Compustat; SICS via SASB CN0403_Multiline-and-Specialty_Brief and SASB CN0501_ApparelAccessoriesFootwear_Brief; Syntax

The result is the ability to build risk groups that capture not only sustainability risks but broader businesses risks, as well. Further, instead of having analysts determine materiality ad hoc, FIS allows Syntax to build algorithmic queries that capture decision-making, ensuring the consistency of the materiality model and further aligning with the rules-based values of passive investing.

A Consistent Approach to Governance

While much attention has been paid to the environmental and (to a lesser extent) social aspects within ESG, considerably less has been paid to the governance pillar. Within ESG, governance stands apart for a number of reasons. First, the notion of looking at extra-financial factors around governance practices is hardly limited to ESG; active managers have integrated governance practices into their investment decisions for decades outside of an ESG context. Large active investors often scrutinize management and boards, even going so far as to build investment models based on the psychological profiles of CEOs [3]. Second, unlike environmental and social considerations, governance is universally material to the financial performance of companies – that is, governance practices are financially material regardless of industry. Thus, investors cannot rely upon materiality frameworks like SASB to help us settle upon what metrics to consider.

As a result, existing governance scoring methodologies tend to take into account a vast range of metrics, with some frameworks considering more than 600 metrics. These models take into account everything from the number of meetings attended in person by board members to policy on golden parachutes. Sometimes the metrics considered have conflicting aims. Take the example of staggered boards, which considers whether board members all come up for election each year (unstaggered) or whether only a fraction of the board is up for election each year, with those voted in holding multi-year terms (staggered). Unstaggered boards may promote shareholder rights in that they allow shareholders to hold board members accountable each year, but at the same time unstaggered boards may discourage long-term decision-making amongst board members [4]. Shareholder rights is a core tenant of ESG investing, but so is long-termism. How should an ESG investor weigh these conflicting metrics in calculating an ESG score?

Syntax’s approach to measuring good governance seeks to align with the goals of the environmental and social pillars of ESG and remain consistent with the tenants of responsible investing. The Syntax governance model aggregates just 19 governance metrics grouped into four categories: ethics, diversity, long-termism, and shareholder democracy. These pillars were developed using industry frameworks including the Investor Stewardship Group’s corporate governance principles for U.S listed companies, and academic research from institutions including Oxford University and Harvard Business School. Metrics that are contradictory across these pillars, like staggered boards, are not considered.

Pillar 1 – Ethics

Ethical corporate behavior on environmental, social and governance issues is aligned with the spirit and goals of ESG investing that rewards good corporate stewardship. There is also strong evidence that good ethics preserves shareholder value in that it avoids share-price shocks around corporate scandals [5,6,7,8].

Pillar 2 – Diversity

Diversity is also aligned with the Social pillar of ESG in that it rewards equitable corporate social behavior that takes into account a broad range of stakeholders and has larger societal benefits. There is also strong evidence that promoting diversity in the workplace leads to improved innovation and better decision-making overall [9,10].

Pillar 3 – Long-Termism

Long-termism, or measures that shift corporate boards’ and management’s focus towards long-term profits, is also highly aligned with the goals of ESG investing, which believes that corporations will thrive over the long run if they are good stewards for the planet and for society. Many of the risks that ESG investing takes into account will be borne out over the long term. The long-termism governance metrics ask if corporate governance incentive structures are aligned with the long-term investor.

Pillar 4 – Shareholder Democracy

Shareholder democracy ensures structures are in place at a company so that investors can act as engaged shareholders by proposing shareholder resolutions, exercising proxy voting and holding board members accountable for decisions. Shareholder engagement is a cornerstone of ESG investing, and, we believe, will be increasingly important in pushing companies to disclose environmental and social risks and shift their focus to the long term. In short, shareholder engagement can be a powerful tool to improve a company’s ESG performance.

Without clear guidance on the materiality of governance metrics, governance models can often lose sight of their ultimate aim. The Syntax governance model attempts to build a transparent framework for corporate governance that is aligned with the broader goals and spirit of responsible investing. It also has the added benefit of improving transparency over other governance models, as it is simplified and easy to communicate to investors in a methodology document.

Business Risk Diversification

Idiosyncratic Risk Diversification

By construction, cap weighted indices are concentrated in the largest companies. Most ESG indices cut out the worst performing companies by ESG score. For a number of reasons, including resource constraints on smaller companies and historical lack of incentive for robustly reporting ESG performance, ESG scores tend to correlate with size, with larger companies performing better. This leads to considerable size bias and single-company bias in cap weighted ESG even when compared against their already biased benchmarks. For example, as of December 31st, 2019, the MSCI USA ESG Leaders index had 29% weight in its top 10 holdings, whereas its non-ESG benchmark the MSCI USA Index had 21% in its top 10 holdings. In comparison, the Syntax ESG index has 14.4% in its top 10 holdings vs. the S&P 500, which has 23.9% in its top 10 holdings. This is not a problem particular to MSCI’s indices. It is common among cap weighted ESG indices. Through diversifying business risk, Syntax stratified weight keeps the weight of individual securities from ballooning to the levels seen with cap weight.

Sector and Industry Diversification

There is also sector and industry bias in cap weighted ESG indices even when compared to their already biased benchmarks. For example, the S&P 500 ESG Index’s largest sector is IT at 25% of index weight compared with the S&P 500, which holds 23% in IT. Bias exists below the sector level as well. For example, within IT, the MSCI USA ESG Leaders Index holds 10x less weight in hardware companies than its non-ESG benchmark and software companies account for 11.5% of total index weight compared with just over 7% for its benchmark. Elsewhere, the MSCI ESG Leaders Index holds over 2x weight in household and personal products compared to its benchmark. Again, this is a problem not limited to one specific index or index issuer, but common among cap weight ESG indices. The Syntax Stratified LargeCap ESG Index is constructed to ensure that all sector and industry weights mirror those of the Syntax Stratified LargeCap Index, which is designed to neutralize business risk through equal allocations to sectors, equal allocation to sub-sectors within each sector, and equal exposure to industries within sub-sectors.

Enhance Diversification Lost in Smaller Investment Universe

In screening out poor-performing ESG companies, ESG indices shrink the investable universe and decrease diversification. In theory, the premium gained by investing in better ESG companies should more than make up for the lost diversification premium. However, the burden is entirely on the ESG factor to make up this ground. The theory for stratified weight’s outperformance is that better diversification through weighting choices helps make up for the diversification lost with a smaller universe. Further, there is evidence that this stratified weight premium can be applied in combination with traditional factor premia without dampening the effect of the factor. This logic extends to treating ESG as a factor.

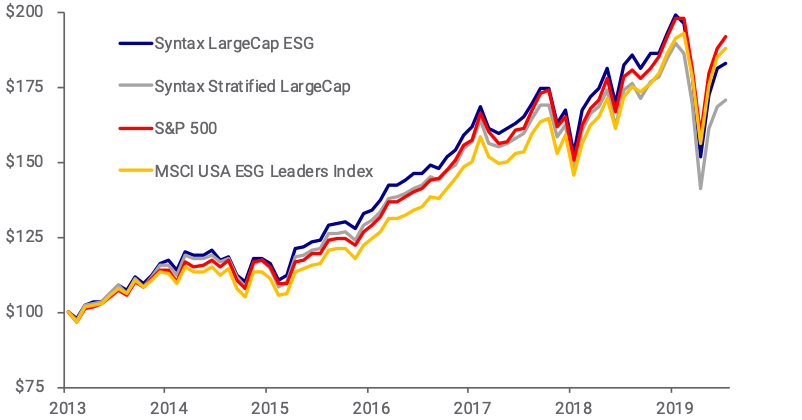

Performance

With limited history available on ESG indices given data availability constraints, it is difficult to draw conclusions from any ESG backtest. However, the Syntax Stratified LargeCap ESG Index has outperformed its Syntax Stratified LargeCap benchmark since the inception of the backtest on 12.20.2013, indicating the value of the Syntax ESG model. However, during this limited sample period, both the Syntax Stratified LargeCap and Syntax Stratified LargeCap ESG indices have underperformed the momentum-heavy S&P 500. We expect a more diversified strategy like Stratified Weight to have relative underperformance in high-momentum market environments, like what we have experienced during this period, where mega-cap stocks have substantially outperformed the rest of the S&P 500. However, this outperformance has led to even further single-stock and business-risk concentrations, especially in technology, that leave cap weighted indices vulnerable to momentum reversals in the future.

Exhibit 3:

Source: Syntax. Total return from 12.20.2013 – 6.30.2020; periods longer than one year have been annualized. Performance does not reflect fees or implementation costs as an investor cannot directly invest in an index. Please see important disclaimers on regarding backtested data prior to inception

Florian Berg, Julian F. Koelbel, Roberto Rigobon. “Aggregate Confusion: The Divergence of ESG Ratings.” MIT Sloan, University of Zurich August 15, 2019.

Subramanian, Guhan. “Corporate Governance 2.0”, Harvard Business Review, March 2015.

Muoghalu, M. I., Robison, H. D., & Glascock, J. L. “Hazardous waste lawsuits, stockholder returns, and deterrence.” Southern Economic Journal, 57(2): 357. 1990.

Karpoff, J. M., Lott, J., & Wehrly, E. W. “The reputational penalties for environmental violations: Empirical evidence.” Journal of Law and Economics, 48(2): 653–675. 2005.

Karpoff, J. M., & Lott, J. “Reputational penalty firms bear from committing criminal fraud.” Journal of Law and Economics, 36: 757–802. 1993.

Karpoff, J. M., Lee, D. S., & Martin, G. S. “The cost to firms of cooking the books.” Journal of Financial and Quantitative Analysis, 43(03): 581–581. 2008.

Gao, Huasheng and Wei Zhang. “Employment Nondiscrimination Acts and Corporate Innovation.” Management Science 63: 2982-2999. 2017.

Dezső , Cristian L., & Gaddis Ross, David “Does Female Representation in Top Management Improve Firm Performance? A Panel Data Investigation.” Strategic Management Journal 33(9): 1072-1089. 2012.

Disclaimers

Past performance is no guarantee of future results. All performance presented prior to the index inception date is backtested performance. Backtested performance is not actual performance, but is hypothetical. The inception date of the Syntax Stratified LargeCap ESG Index is July 31, 2020. The inception date of the Syntax Stratified LargeCap Index was December 27, 2016. The backtest calculations are based on the same methodology that was in effect when the index was officially launched. However, back-tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index. Charts and graphs are provided for illustrative purposes only.

The Syntax Stratified LargeCap Index (“the LargeCap Index”) is the property of Syntax, LLC, which has contracted with S&P Opco, LLC (a subsidiary of S&P Dow Jones Indices LLC) to calculate and maintain the LargeCap Index. The LargeCap Index is not sponsored by S&P Dow Jones Indices or its affiliates or its third party licensors (collectively, “S&P Dow Jones Indices”). S&P Dow Jones Indices will not be liable for any errors or omissions in calculating the LargeCap Index. “Calculated by S&P Dow Jones Indices” and the related stylized mark(s) are service marks of S&P Dow Jones Indices and have been licensed for use by Locus Analytics, LLC. S&P® is a registered trademark of Standard & Poor's Financial Services LLC (“SPFS"), and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). The Syntax Stratified LargeCap ESG Index (“the ESG Index”) is the property of Syntax, LLC, which has contracted with S-Network Global Indexes, Inc. to calculate and maintain the ESG Index. The ESG Index is not sponsored, endorsed, sold or promoted by S-Network Global Indexes, Inc. and S-Network Global Indexes, Inc. makes no representation regarding the advisability of investing to track the Index. Syntax®, Stratified®, Stratified Indices®, Stratified Weight™, and Locus® are trademarks or registered trademarks of Syntax, LLC and its affiliate Locus, LP. FactSet® is a registered trademark of FactSet Research Systems, Inc.

Index performance does not represent actual fund or portfolio performance and such performance does not reflect the actual investment experience of any investor. An investor cannot invest directly in an index. In addition, the results actual investors might have achieved would have differed from those shown because of differences in the timing, amounts of their investments, and fees and expenses associated with an investment in a portfolio invested in accordance with an index. None of the Syntax Indices or the benchmark indices portrayed herein charge management fees or incur brokerage expenses, and no such fees or expenses were deducted from the performance shown; provided, however that the returns of any investment portfolio invested in accordance with such indices would be net of such fees and expenses. Additionally, none of such indices lend securities, and no revenues from securities lending were added to the performance shown.

The S&P 500® Index is an unmanaged index considered representative of the US mid- and large-cap stock market. The S&P 500® Equal Weight Index is an equal-weight version of the S&P 500® Index. The Barclays US Investment Grade represents primarily investment-grade corporate bonds within the Barclays U.S. Aggregate Bond Index. Benchmark data for the S&P 500 and S&P 500 Equal Weight Indices is provided by S&P Dow Jones through FactSet®

This report is for informational purposes only and is not intended to be, nor should it be construed or used as an offer to sell, or a solicitation of any offer to buy, any security. Additionally, the information herein is not intended to provide, and should not be relied upon for, legal advice or investment recommendations. You should make an independent investigation of the matters described herein, including consulting your own advisors on the matters discussed herein. In addition, certain information contained in this report has been obtained from published and non-published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such information is believed to be reliable for the purpose used in this factsheet, such information has not been independently verified by Syntax and Syntax does not assume any responsibility for the accuracy or completeness of such information. Syntax LLC, its affiliates and their independent providers are not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein.

This report and the information herein may not be reproduced (in whole or in part), distributed or transmitted to any other person without the prior written consent of Syntax. Distribution of Syntax data and the use of Syntax indices to create financial products requires a license with Syntax and/or its licensors. Investments are not FDIC insured, may lose value and have no bank guarantee.